Demystifying Blockchain-Supported Smart Contracts

By Chris Howard and Steve McNew, FTI Consulting

Highly capable connected technology has emerged in recent years and is on track to disrupt the traditional pharmaceutical industry. A smart contract is a tool that automatically executes the agreed upon terms, while simultaneously facilitating business and decreasing risk. Promising increased accuracy, transparency, and security, smart contracts and blockchain technology are the next steps in the evolution of secure data transaction. Companies in the pharmaceutical industry, and their supply chains, will be forced to adapt their operations to keep up with these generational changes in order to competitively deliver services and treatments in the future.

Currently, serialization and track and trace requirements are the predominant industry practices, but their execution is manual and disjointed.1 In addition, the ability to confirm a medicine’s end-to-end provenance is becoming an increasingly important aspect of delivering medicines in a safe and trusted manner. With the deployment of distributed ledgers and blockchain technology, these capabilities are simplified and can operate with a higher level of precision.

A distributed ledger technology (DLT), or blockchain, is protected by cryptography. A network of nodes maintains the ledger of information without complete trust between other nodes. As long as a majority of the nodes confirm the entries (“blocks”), then the entry can be posted to the ledger (“chain”) as mandated by the governing rules, and the information will be posted and stored on the blockchain as trusted and reliable.1

The self-executing nature of smart contracts makes it well suited for the pharmaceutical industry. Distributed ledgers have the most success in environments that prioritize privacy, efficiency in sharing information, and data accuracy. Creating a secure environment, automated confirmations can be performed to ensure the validity and completion of the agreement before the contract is executed.

Users have confidence in the distributed ledger’s conditional (“IF, THEN”) logic that forms the foundation of the smart contract’s self-executing code detailing the operational terms of an agreement. Through intelligent process automation, the blockchain streamlines the interactions within the supply chain, allowing for2:

- Automatic payment remittance when a shipment is received

- Returning damaged goods (e.g., medication or therapy stored or transported at the wrong temperature) and initiating relevant quality-control processes automatically

- Lot traceability that can be used to perform recalls

- Detecting product diversion while the product is enroute

Processes that historically have taken hours, days, or even weeks can be validated and executed immediately with smart contracts. Exceptions are automatically identified and flagged, driving the formation of a true control tower.3

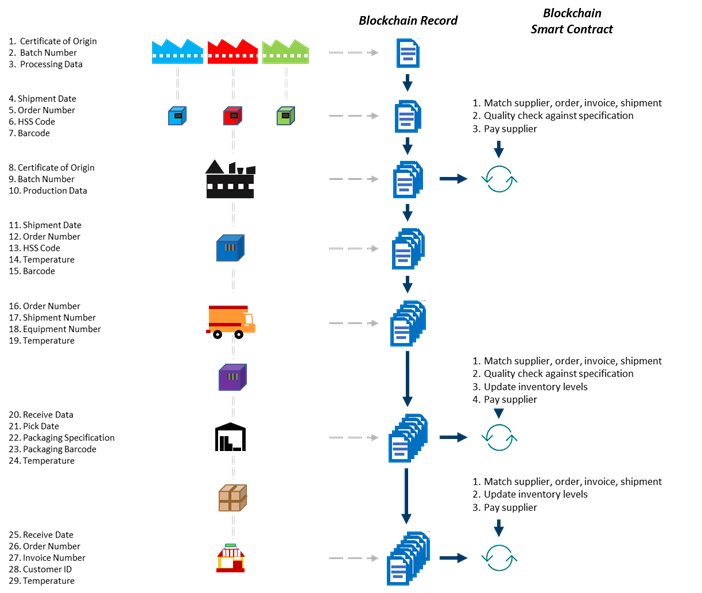

Smart contracts facilitate secure transactions between multiple parties while providing security and transparency to patients and healthcare professionals so treatment can be planned and safely administered. Below is a representation that illustrates how the blockchain record tracks and maintains interactions across the end-to-end supply chain. Blockchain intelligently incorporates critical components associated with managing patients, allocating resources, and ensuring regulatory compliance. These components are recorded and stored so they are immutable but also easily accessed when necessary.4

Figure 1: An example of how blocks relate to chains in a pharmaceutical manufacturing and distribution environment

Incorporating the blockchain into an existing network may seem like a daunting task, but by outlining a robust implementation strategy and aligning the solution architecture so that it sufficiently addresses the needs of the business, companies can effectively leverage smart contracts in their supply chains.

When starting to construct a blockchain, it is important to first identify the systems and processes the blockchain platform will need to support. With this, the development team will be able to understand the use cases for the blockchain and ensure that critical functions are supported.

The next step is to determine the functional areas and data sets required for utilization or tracking purposes. This is important so that the blockchain can integrate with and leverage the information from the current processes.

Companies should then evaluate whether to use an existing platform or develop a blockchain platform in-house. Both have their benefits and disadvantages, but rollout time, cost, and customizability may play a role in the company’s final decision. Once a solution is implemented, the company can take steps to continue scaling and make performance improvements and platform updates as they see fit.

Ultimately, the potential benefits of investing in a robust blockchain solution far outweigh the negatives. With a focused development and implementation plan and forward-looking partners, pharmaceutical companies looking to modernize their supply chains and be competitive in the marketplace will leverage smart contracts as a foundational element in how they do business. Below are three tips as you implement your blockchain solution.5

1. Obtain Executive Buy-In By Appealing To Business Needs & Company Culture

Many teams may find themselves in a situation where implementing a blockchain solution is the logical next step in the company’s supply chain evolution. When looking to obtain executive buy-in, team members should connect the advantages of smart contracts to the company culture. Maybe the team you are on values innovative approaches to solutions, or maybe it is imperative that recorded transactions are incorruptible. Whatever it is, the advantages of blockchain can be prioritized in many ways. Teams should speak to how this technology aligns with the company’s overall strategy and vision for the future, showing how these tools supplement initiatives that are already being invested in. Teams should then clearly communicate the business case and a practical implementation timeline. After the initial idea proposal, strong cases are reinforced by a succinct execution plan, followed with quantifiable metrics that show how the technology improves the supply chain. Teams should conduct and incorporate additional research into their initiatives, highlighting the increased uptick in blockchain adoption in their specific industry, or highlighting the time and cost savings of blockchain processes against traditional processes, in order to reinforce their position.

2. Evaluate Industry Blockchain Trends

Teams that are not ready to make the jump to an entirely blockchain supported solution should follow trends in the industry through publications and industry presentations. These teams should reevaluate when it will make sense to invest in a blockchain solution on a semi-annual or annual basis. This allows organizations to focus on and refine their processes so when it is time to make the jump to an entirely built out blockchain ledger, they can build their solution so it fits the exact criteria required to react to and address the company’s needs.

3. Recruit A Blockchain Expert You Can Trust

When the team is ready to recruit a blockchain expert, it is important to find someone who, in many ways, reflects the qualities of the blockchain itself. This individual should be able to communicate clearly, expertly simplifying complex ideas into terminology and verbiage that can be understood by executives and leadership. The individual should understand the regulatory guidelines for the technology they work with and the industry they operate in. And most importantly, the potential new team member should be continuously adaptive to new information in the industry, tracking how innovation in the blockchain can benefit the company and following how the competition leverages smart contracts and the benefits they are realizing.

Pharmaceutical companies in the future will rely on distributed ledgers and smart contracts to facilitate transactions across the entire value chain. Driven by technological advancements, increased adoption, and universal connectivity, an integrated blockchain allows pharmaceutical companies to benefit from the advanced capabilities of this new technology when managing and delivering lifesaving products. While the initial implementation cost can be steep, hindering some organizations from adopting blockchain sooner, organizations will see a return on invested capital in terms of time saved, reduced costs, and risk mitigation.

Acknowledgments

The authors would like to thank Joe Slota, Rick van der Vegte, and Andrew Caruso for providing valuable input on this article.

References

1. Transforming The Life Sciences Supply Chain Through Blockchain;

https://www.worldpharmatoday.com/articles/transforming-the-life-sciences-supply-chain-through-blockchain/

2. 10 FAQs About Blockchain and Life Sciences – What are Smart Contracts. Law of the Ledger, Sheppard Mullin.

https://www.lawoftheledger.com/wp-content/uploads/sites/777/2018/08/10-FAQs-About-Blockchain-and-Life-Sciences-Article-0818.pdf

3. FDA DSCSA Blockchain Interoperability Pilot Project Report, p. 7;

https://www.ibm.com/downloads/cas/9V2LRYG5

4. 10 FAQs About Blockchain and Life Sciences, p. 9. Law of the Ledger, Sheppard Mullin.

https://www.lawoftheledger.com/wp-content/uploads/sites/777/2018/08/10-FAQs-About-Blockchain-and-Life-Sciences-Article-0818.pdf

5. 10 Advantages of Using Smart Contracts

https://medium.com/@ChainTrade/10-advantages-of-using-smart-contracts-bc29c508691a

About The Authors:

Chris Howard serves as a leader within the Operations and Supply Chain Management offering within Health Solutions, bringing deep technology experience which takes on the daunting task of propelling organizations into the future. He has over 10 years of experience providing strategy, technology transformation, operational, and financial services to global companies, helping them achieve their strategic vision. His experience ranges across multiple industries with a focus on life sciences and multiple operational functions such as engineering, facilities, manufacturing, logistics, distribution, control tower, sourcing and procurement, and end-to-end supply chain strategy.

Steve McNew has served as strategic advisor, consultant, engagement manager, and project manager to corporations of all sizes and their legal counsel in a multitude of matters. He provided strategic consulting, e-discovery, information management, and technology services to the world’s largest research-based pharmaceutical company for more than six years with matters involving contract disputes, multiple drug cases, and general litigation. McNew regularly presents at industry events on best practices for e-discovery, data security, and information governance.

The views expressed herein are those of the author(s) and not necessarily the views of FTI Consulting, Inc., its management, its subsidiaries, its affiliates, or its other professionals. FTI Consulting, Inc., including its subsidiaries and affiliates, is a consulting firm and is not a certified public accounting firm or a law firm