Hormuz Deal Brings Cautious Relief To Pharma Packaging Supply Chains

By Jose Saiz de Omeñaca

The disruption of sea transit through the Strait of Hormuz quickly became one of the most serious supply chain challenges in 2026. While public attention has focused for the most part on rising oil and gas prices, the crisis also affected the availability of raw materials used in pharmaceutical manufacturing, healthcare packaging, and medical technology.

This week the U.S. and Iran signed a memorandum of understanding to end the war and reopen of the strait. The MOU opens a 60-day period of negotiations between the two countries. While reopening the strait during that window is part of the agreement, just how freely traffic will resume, and for how long, remains unclear.

The normalization of transit through the strait would help reduce volatility in energy and chemical markets. In the first few hours alone, the price of crude oil fell by 10%, which will help alleviate tensions in global supply chains and foster a more stable cost environment for industrial consumers in Europe and the United States. However, the supply of petrochemical raw materials will not be fully restored in the next several weeks due to damaged facilities in producing countries. Beyond that, energy and fertilizer shipments will receive preference over plastics and chemicals.

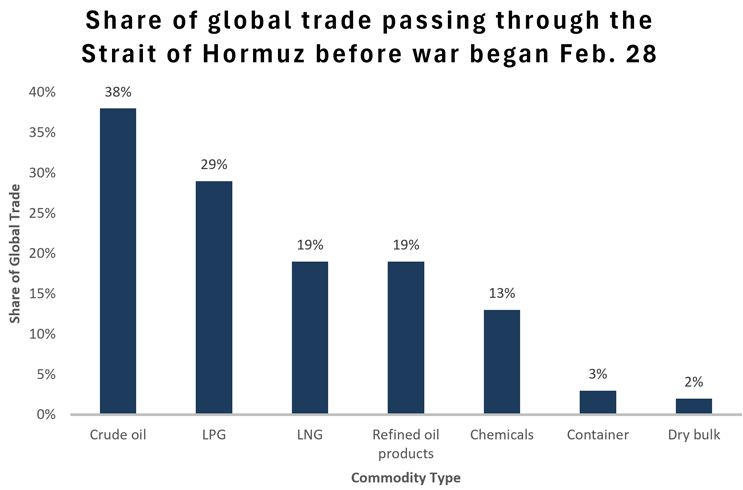

The strait is one of the world’s most important trade corridors, counting around 8% of the global maritime trade transiting key chokepoints. Apart from oil and gas, the region exports large volumes of petrochemicals, industrial gases, and chemicals, essential products for pharma production. As conflict involving Iran and the U.S. intensified and maritime traffic sharply declined, pharmaceutical manufacturers began experiencing rising transportation costs, delayed shipments due to the need to find alternatives routes, and tightening supplies of key materials.

The strait serves as the primary export route for Gulf nations (Saudi Arabia, Qatar, Kuwait, and United Arab Emirates), but its importance to industrial raw materials and chemical supply chains has received less attention.

Some critical commodities such as methanol, sulfur derivatives, and aluminum are facing scarcity, increasing risks in medicine production and healthcare systems worldwide. Pharmaceutical manufacturing depends on highly regulated supply chains, and companies cannot easily substitute suppliers or materials without extensive approval processes.

As tensions involving Iran increased, many shipping companies reduced or suspended traffic through the strait due to military risks and rising war-risk insurance premiums.

![]()

Source: UN Trade and Development (UNCTAD)

India and China produce around 40% of essential APIs and 50% of non-essential APIs. India produces around 20% of generic medicines and depends heavily on imported industrial chemicals connected to gulf supply chains.

Source: UN Trade and Development (UNCTAD)

The crisis has exposed pharmaceutical manufacturing and supply chains' vulnerability to geopolitical instability. The COVID-19 pandemic taught us important lessons about the dangers of concentrated sourcing and lean inventory systems. The Hormuz disruption reinforced the need for greater supply chain resilience and new strategies across the pharma and healthcare industries.

As mentioned previously, one of the risks for the pharmaceutical industry involves petrochemical feedstocks. Methanol, extensively used in solvents and pharmaceutical intermediates, is heavily dependent on gulf exports. Around one-third of global seaborne methanol trade normally passes through the strait. Rising methanol prices could increase manufacturing costs for generic medicines, antibiotics, and specialty pharmaceutical products.

Another important concern is monoethylene glycol (MEG), which is used in healthcare plastics, sterile packaging materials, and pharmaceutical containers. Packaging shortages could become a major issue because pharmaceutical packaging must meet strict regulatory standards.

Helium shortages also emerged as a serious healthcare challenge. Qatar supplies nearly one-third of the world's helium. Helium is essential for MRI machines, laboratory cooling systems, and semiconductor manufacturing.

Another raw material affected is aluminum. Exports from the Persian Gulf region are around 10% of global primary aluminum, which is widely used in pharmaceutical blister packs, sterile foil packaging, and medical devices. Rising aluminum costs may increase packaging expenses and create additional supply bottlenecks.

Transportation challenges are worsening the situation. Shipping companies rerouted vessels away from the gulf, increasing transit times, freight costs, and insurance expenses. Congestion at alternative ports slowed deliveries and added further pressure to already strained supply chains.

Pharmaceutical manufacturers operating lean inventory systems are particularly vulnerable. Many companies are now increasing safety stock levels and seeking alternative suppliers to reduce risk exposure. However, larger companies are better positioned to secure long-term contracts, while smaller manufacturers may struggle with rising costs and limited supply availability.

The crisis has become a broader industrial and healthcare supply chain challenge with significant implications for pharmaceutical manufacturing and global medicine availability.

The pharmaceutical sector depends heavily on globally interconnected networks for chemical feedstocks, packaging materials, and medical technologies.

Over the next several months, pharmaceutical and healthcare companies are likely to face continued volatility in raw material pricing, transportation costs, and supplier reliability. Healthcare systems may also experience rising operational costs linked to diagnostics equipment, packaging shortages, and delayed medicine production.

At the same time, the crisis is accelerating a shift toward more resilient supply chain strategies. Pharmaceutical manufacturers are increasingly expected to diversify sourcing, regionalize production, and strengthen inventory management to reduce dependence on vulnerable trade routes.

About The Author:

Jose Saiz de Omeñaca is a pharmaceutical executive with 25 years of experience in procurement, supply chain, and operations in pharma, CDMO, industrial, and retail environments, with experience in medium and large companies, as well as in transformation and operational improvement projects. He received a Master of Business Management from Instituto de Empresa (IE) and Master of Supply Chain at Universidad Carlos III de Madrid. He serves as an expert with UNECE/UNCEFACT. Email him at josesaizmonzon@yahoo.com. Connect with him on LinkedIn.

Jose Saiz de Omeñaca is a pharmaceutical executive with 25 years of experience in procurement, supply chain, and operations in pharma, CDMO, industrial, and retail environments, with experience in medium and large companies, as well as in transformation and operational improvement projects. He received a Master of Business Management from Instituto de Empresa (IE) and Master of Supply Chain at Universidad Carlos III de Madrid. He serves as an expert with UNECE/UNCEFACT. Email him at josesaizmonzon@yahoo.com. Connect with him on LinkedIn.